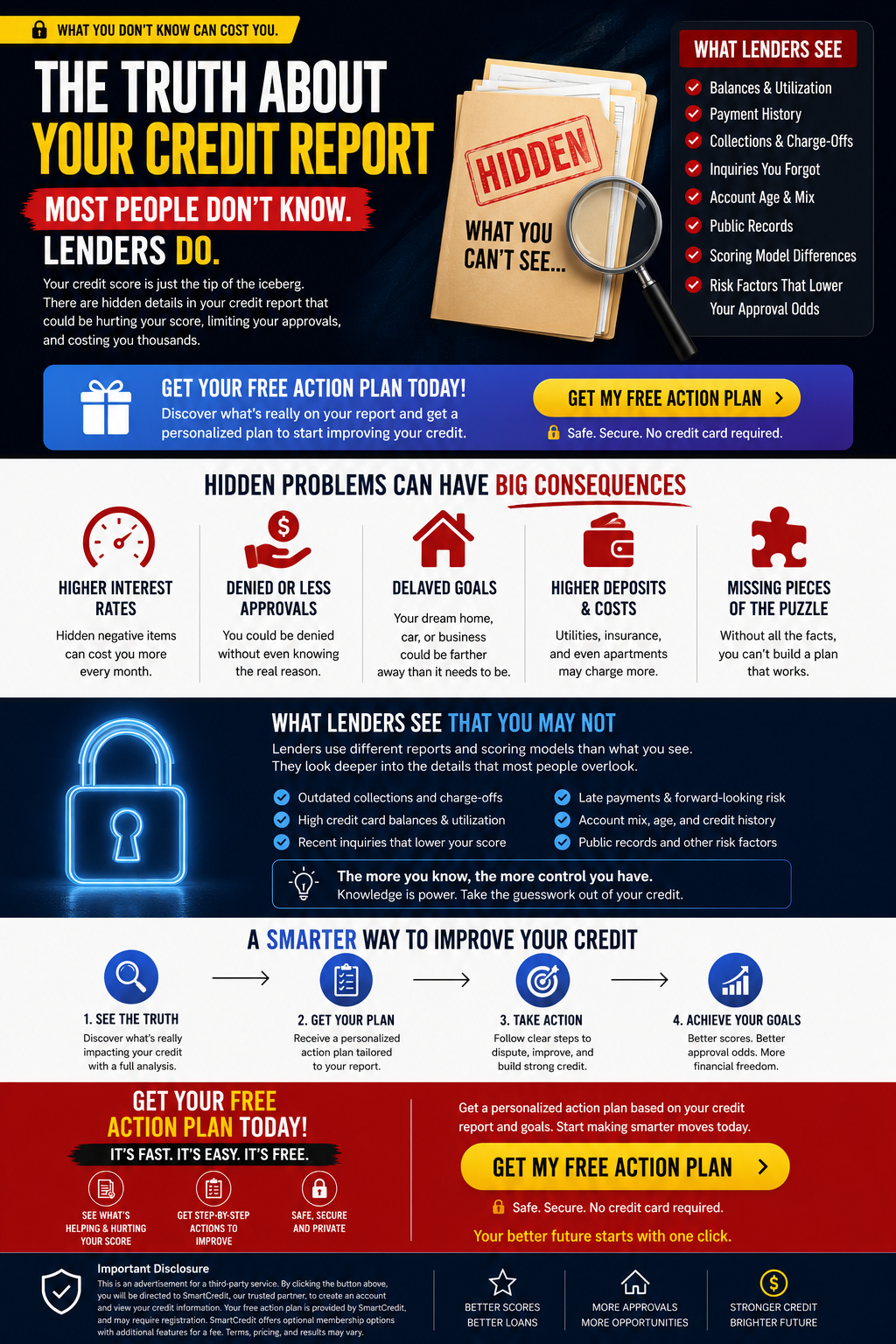

What many consumers notice

- The score shown in an app

- Whether accounts appear open or closed

- A basic list of debts

- Recent score changes

Your credit score is only one part of the story. Lenders may also review balances, payment history, utilization, collections, inquiries, account age, and other risk factors.

See the full picture before you apply.

Many consumers focus only on a single score. A lender may look deeper into the information behind that score before deciding whether to approve an application and what terms to offer.

Risk factors on a report may affect the rate, deposit, or terms you are offered.

An application can be declined even when the score alone appears acceptable.

Homeownership, a reliable vehicle, or business financing may take longer without a clear plan.

Open each section to learn why it may matter.

Utilization compares revolving balances with available limits. High usage may signal greater risk, even when every payment has been made on time.

Late payments can remain influential for years. Recent or repeated late payments may carry more concern than an isolated older event.

These items may affect scoring and may also influence manual underwriting or approval requirements. Accuracy, age, balance, and status can all matter.

Multiple recent applications can suggest increased borrowing risk. Their effect depends on timing, type of credit, and the scoring model used.

A longer history and responsible use of different account types may help demonstrate consistency, but opening accounts solely to change the mix can create new risks.

Review the information connected to your credit profile.

Identify which factors may be helping or limiting your progress.

Use clear next steps based on your report and financial goals.

Monitor changes and make better-informed credit decisions.

Start by reviewing your credit information and receive a personalized starting plan designed to help you understand what to address first.

Not necessarily. Different lenders may use different credit bureaus, scoring models, versions, and internal approval criteria.

Checking your own credit is generally treated as a soft inquiry and does not have the same scoring effect as a lender's hard inquiry.

No. Credit outcomes depend on the information in your file, the actions taken, timing, creditor reporting, and the scoring model being used.

The action plan may be included with the service, but registration, trial, membership, or optional paid features may have separate terms. Review those terms before enrolling.